Silicon Valley builds with capital abundance, while Emerging Europe builds with capital constraint; that single difference changes everything. Most Central and Eastern European markets are too small to support venture-scale outcomes, and domestic demand rarely creates billion-dollar companies outside a few verticals. This is not a weakness; it is a forcing function. If your home market cannot carry you, your product must.

There is no local monopoly phase, no protected scaling window, and no “we’ll expand internationally later” illusion.

You start global, or you don’t survive, and that pressure produces a very specific founder profile.

The Global-First Reflex Is Structural, Not Aspirational

In Silicon Valley, global expansion is a strategy, whereas in Emerging Europe, it is a default setting. More than 40 of the 53 CEE unicorns generate minimal sales from their domestic markets.

That statistic is not cosmetic; it reflects a different mental model. Products are built in English from day one, distribution strategies assume global channels, and teams are remote-native before remote became fashionable. This eliminates a common Western failure mode: over-optimizing for local validation. CEE founders rarely get the luxury of building something mediocre that works “well enough” at home.

Therefore, global competitiveness is not optional; it is embedded.

Technical Depth Is Not the Advantage. Stress Is.

Everyone talks about engineering strength. Yes, the region has strong mathematics and computer science traditions, and yes, talent density is real, but that is not the differentiator.

The differentiator is that these teams were formed under structural stress.

- Lower capital density.

- Smaller domestic markets.

- Higher geopolitical volatility.

This forces discipline early.

- Teams optimize burn instinctively.

- They validate quickly.

- They kill faster.

Silicon Valley discipline is often learned post-Series B. In Emerging Europe, it is learned pre-seed. That difference compounds over a decade.

The Skype Effect Was Not an Accident

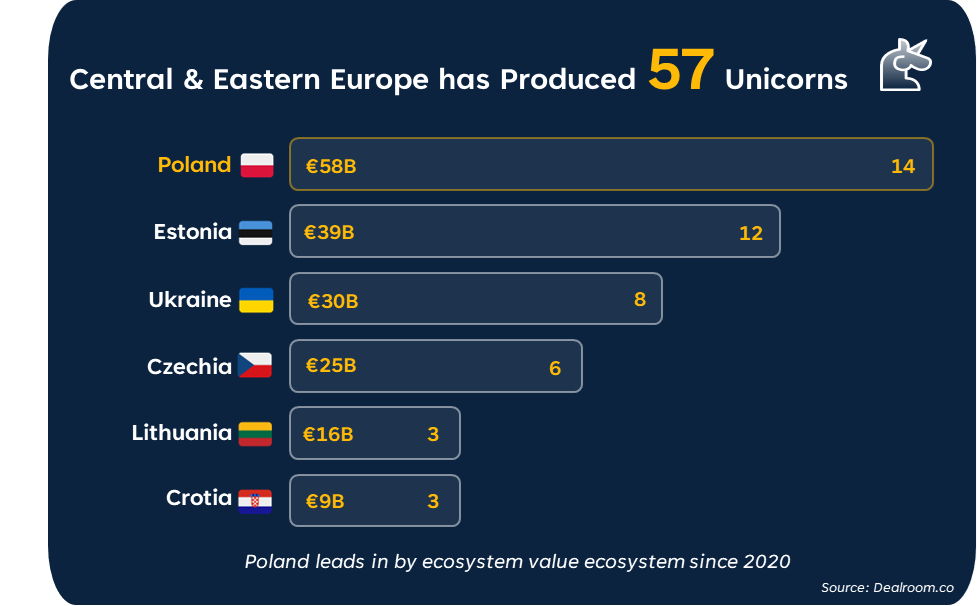

Skype is often referenced as Estonia’s breakout success, but the important story is not the exit; it is the operator recycling. The Skype alumni network seeded dozens of new ventures as capital and ambition circulated locally, ultimately helping Estonia become one of the highest unicorn-per-capita ecosystems in the world.

This is how ecosystems graduate from anomaly to engine: one breakout creates confidence, confidence attracts capital, and capital reinforces ambition. CEE is now operating in that second phase across multiple countries simultaneously.

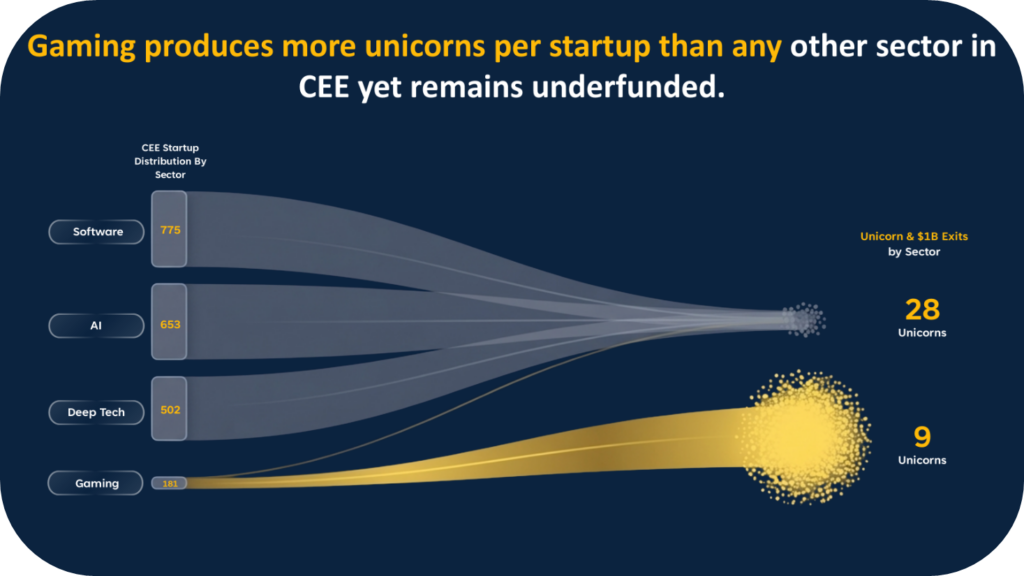

Gaming Reveals the Structural Edge Clearly

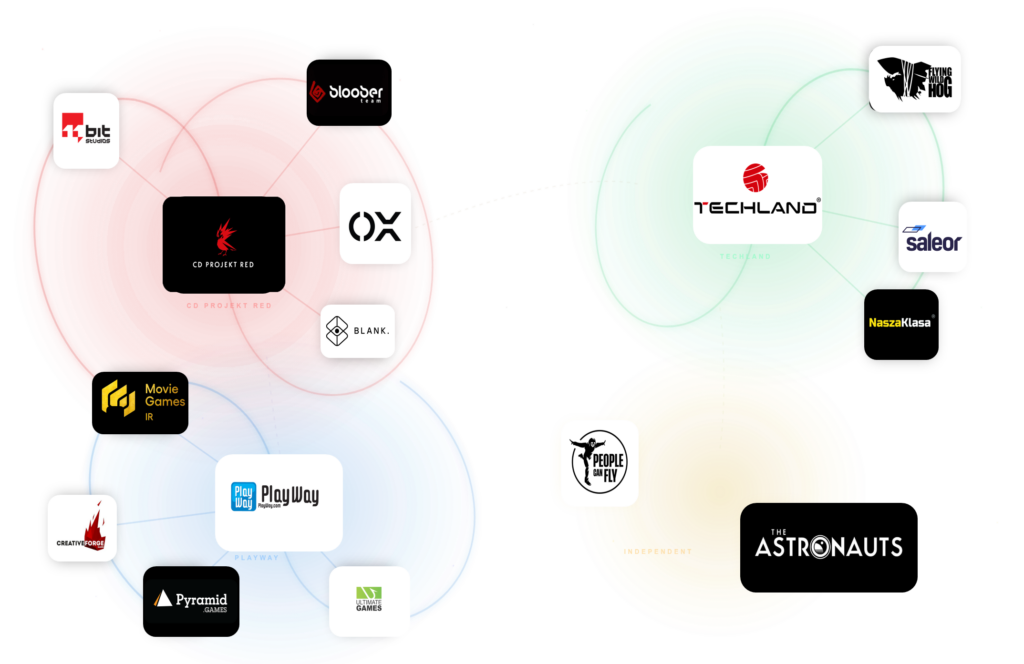

Gaming is a brutal industry defined by global distribution, auction-based user acquisition, and data-driven survival; hence, there is no room for regional mediocrity. CD Projekt built globally dominant IP from Warsaw, and Ukrainian studios have shipped globally competitive titles under extraordinary macro pressure.

These companies did not scale because they dominated Poland or Ukraine; they scaled because they competed internationally from inception. Gaming strips away illusion: you either retain users globally or you disappear, and CEE teams are culturally adapted to that reality.

The Capital Mispricing Window

Here is where it becomes interesting for investors.

Emerging Europe produces globally competitive companies at valuation benchmarks that still reflect regional discounting.

- High technical standards.

- Global-first orientation.

- Lower capital saturation.

That combination creates asymmetry. In ecosystems with capital abundance, valuations price in optionality early, whereas in CEE, optionality is often priced later. This window does not stay open indefinitely. Israel went through it, and Estonia went through it, as valuation convergence follows ecosystem confidence.

The question is not whether Emerging Europe can produce companies at Silicon Valley standards, because it already does. The real question is how long capital continues to treat it as a peripheral market rather than a structurally hardened one. Silicon Valley was built in abundance, while Emerging Europe was built in constraint.

Constraint sharpens, and sharpened ecosystems compound quietly until the market realizes the standards were always there.